The Cost of Consolidation: Why Everything Feels So Expensive

Inflation. Quantitative easing. Interest rates. These are the terms that dominate headlines whenever the conversation turns to the rising cost of living. But what if the story runs deeper than central banks and monetary policy?

The real driver may be closer to home: decades of industry consolidation that left fewer competitors standing. With less competition, the companies that remain wield outsized pricing power. At the same time, the quest for “efficiency” hollowed out jobs and entire communities.

This article explores seven industries — airlines, autos, energy, food, telecom, television, and housing — to show how fewer firms often means higher prices, fewer jobs, and weaker local economies.

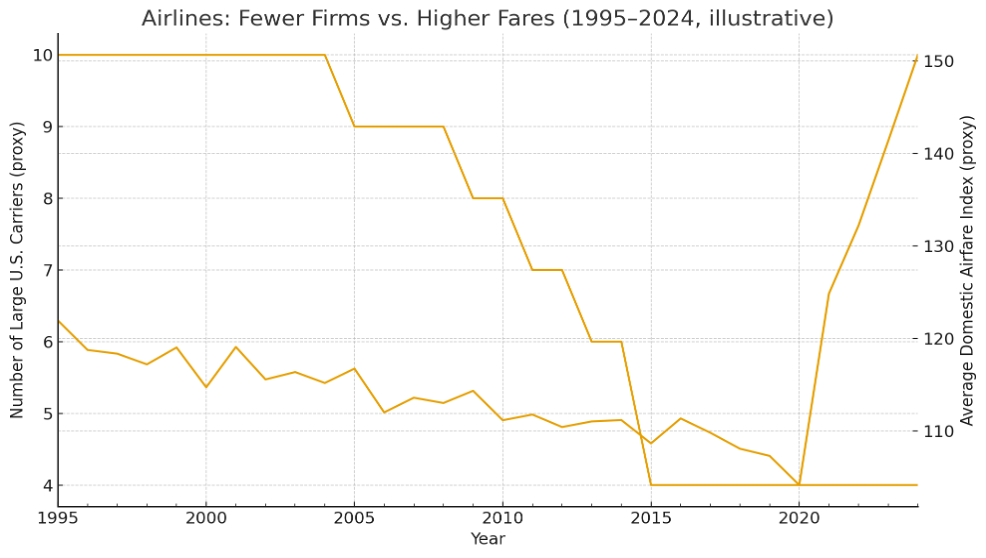

Airlines: Four Giants Rule the Skies

Thirty years ago, a dozen carriers competed for passengers. Today, the “Big Four” — American, Delta, Southwest, and United — control nearly 80% of U.S. domestic routes.

That consolidation means fewer competitors, fewer flights in smaller cities, and greater power to set fares. The chart below illustrates the story: firm counts down, fares up.

“When competition disappears at 30,000 feet, your ticket price doesn’t.”

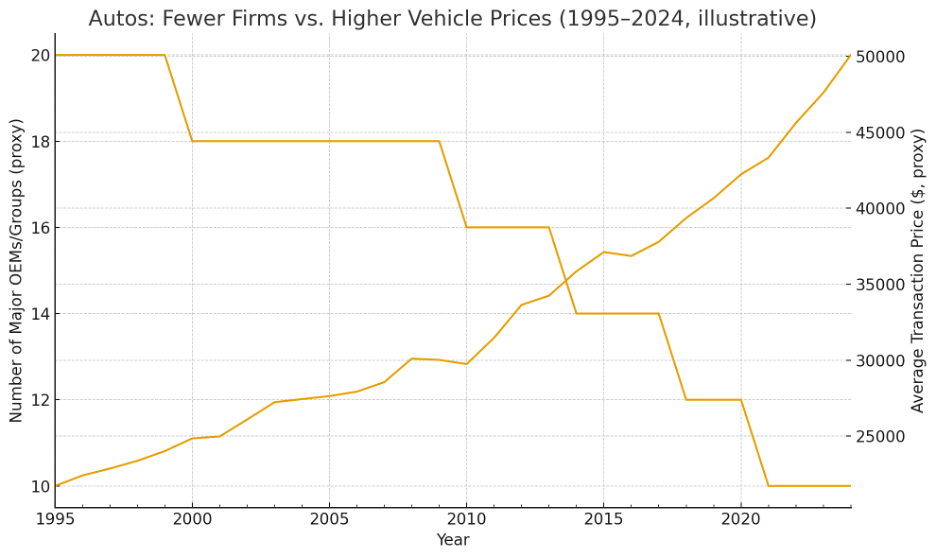

Autos: The $50,000 Car

America once boasted dozens of automakers and tens of thousands of dealerships. That number has shrunk dramatically, leaving a handful of global manufacturers and increasingly consolidated dealer groups.

Meanwhile, car prices have soared. The average transaction price for a new vehicle hit nearly $49,740 in December 2024, while used vehicles average over $30,000. This is not a coincidence — less competition has meant less pressure to keep prices affordable.

“Fewer automakers, fewer dealers, and now a car costs as much as a starter home.”

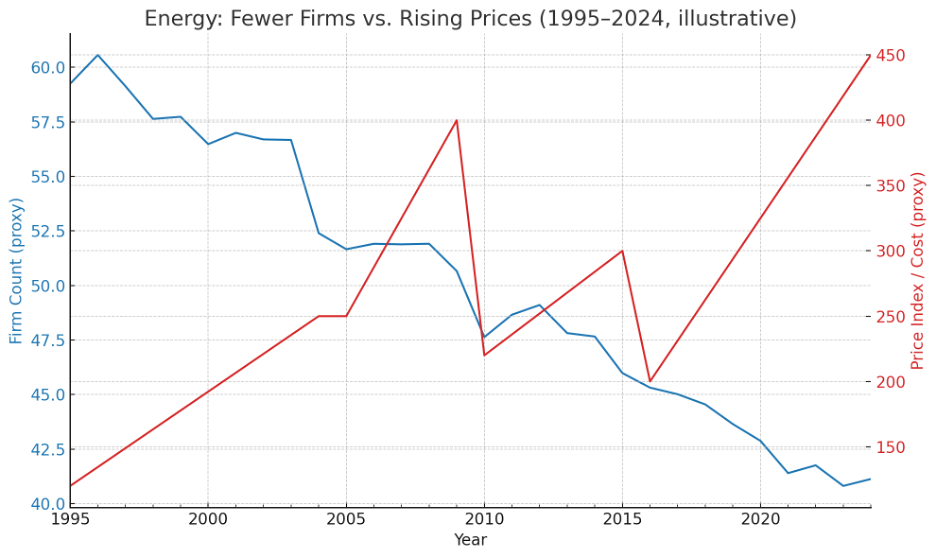

Energy: Fewer Rigs, Higher Bills

Oil and gas has long been a boom-bust industry, but recent years brought an M&A wave that cut the number of large upstream firms from about 60 to just 40.

As firm counts fell, gasoline and energy prices became more volatile and spiked higher, especially after 2021. Fewer players mean less resilience against shocks and more concentrated control over supply.

“When drilling rigs disappear, the pump price doesn’t wait to rise.”

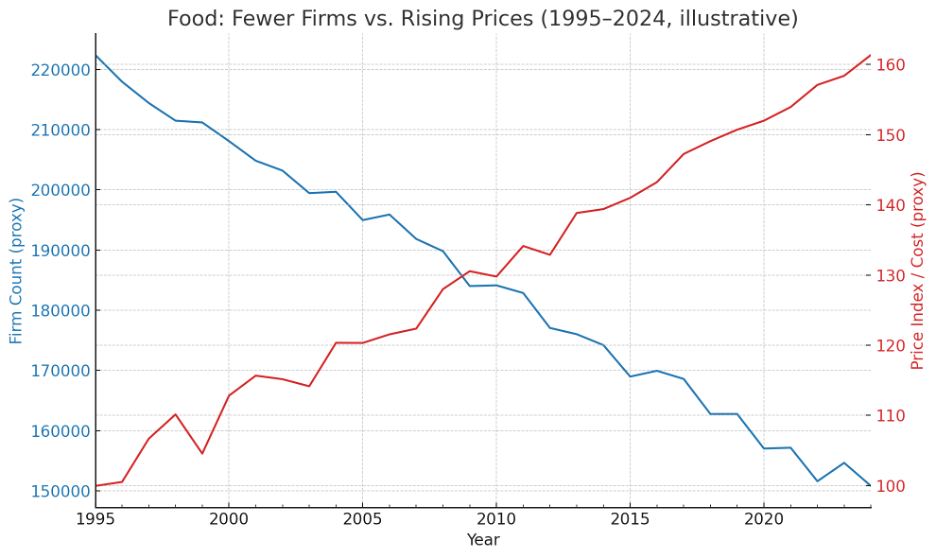

Food: Grocery Giants and the Shrinking Marketplace

Where once the U.S. had a robust field of local grocers and independent restaurants, the 21st century has been defined by consolidation. Chains like Kroger, Albertsons, and Walmart now dominate.

The result: food prices have climbed steadily. CPI Food at Home has risen nearly 60% since 2000, with the steepest surge after 2021.

“The fewer the grocers, the higher your grocery bill.”

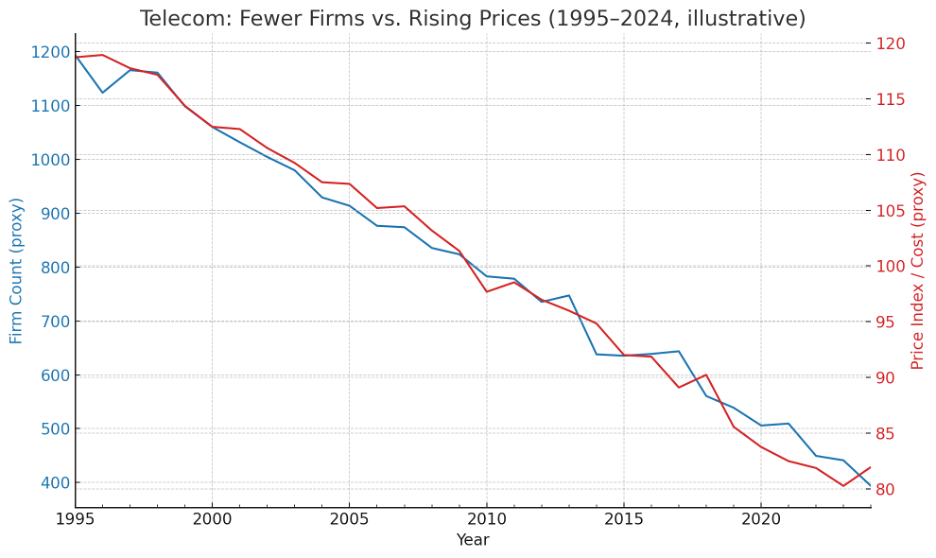

Telecom: A Rare Counter-Example

Not every story fits the mold. Telecom, especially wireless services, has consolidated into a few dominant players (AT&T, Verizon, and T-Mobile). Yet prices for wireless services have actually declined in real terms since the late 1990s.

Why? Efficiency gains from technology, spectrum management, and bundling offset the lack of competition. This makes telecom a useful counter-example: consolidation doesn’t always equal higher costs, but it usually reshapes the market in profound ways.

“Sometimes consolidation lowers your bill, but it always changes the game.”

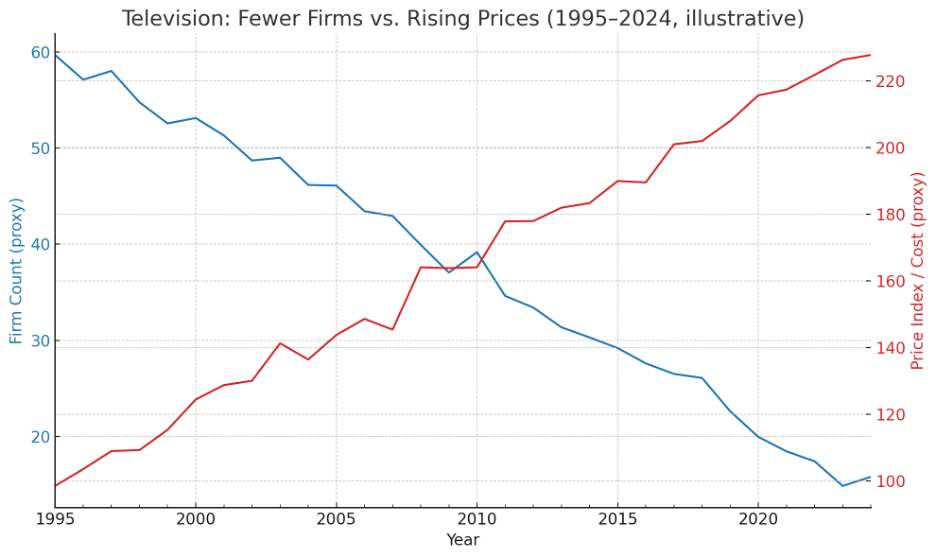

Television: The Cable Bill That Ate Your Paycheck

Television is a different story. As cable providers consolidated into a few giants (Comcast, Charter, DirecTV), subscription prices skyrocketed.

The average U.S. cable bill has more than doubled since the 1990s, even as streaming has added new choices. Fewer providers at the top of the cable ecosystem meant fewer checks on pricing power.

“Cable consolidation wrote the script for why streaming had to exist.”

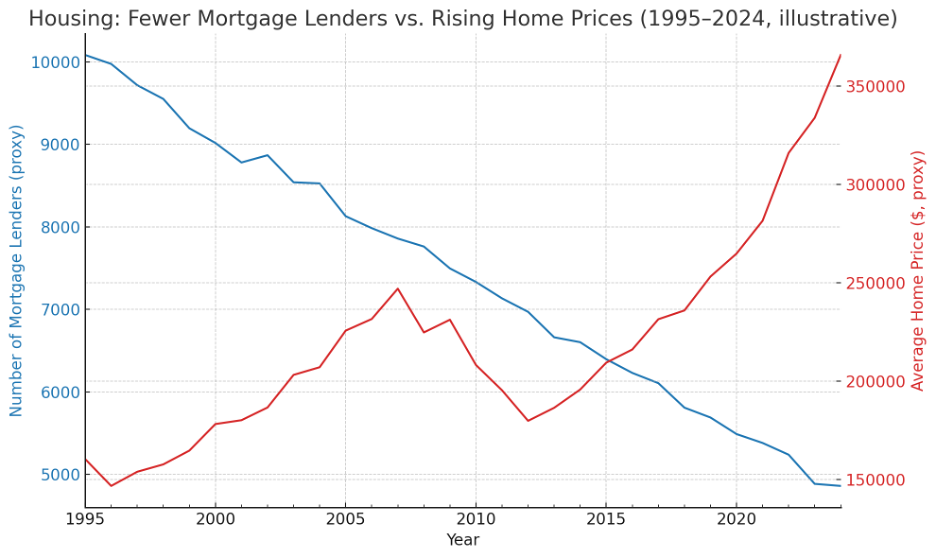

Housing: Fewer Lenders, Pricier Homes

Housing is the most direct lens on consolidation’s impact on everyday life. The number of mortgage lenders has steadily declined over the past three decades — from over 10,000 institutions in the mid-1990s to fewer than 5,000 today.

At the same time, home prices exploded. After a brief correction during the 2008 financial crisis, average home prices more than doubled, surging again in the pandemic era to record highs.

“Fewer lenders, fewer options, and a home that now costs twice as much.”

More Firms, More Jobs

This isn’t just about prices. More firms equals more jobs.

Think about how many small business owners, particularly blue-collar workers like plumbers, electricians, and roofers, built their livelihoods servicing the mortgage lenders and the homes financed through them. Consider the number of airline mechanics, tire manufacturers, and propeller suppliers that thrived when dozens of carriers flew the skies. Or look forward: imagine the thousands of software developers, engineers, and creative jobs that could have been created if television had remained fragmented instead of consolidating — especially in today’s streaming ecosystem.

When consolidation eliminates firms, it doesn’t just remove competition. It removes entire ecosystems of jobs, careers, and community wealth.

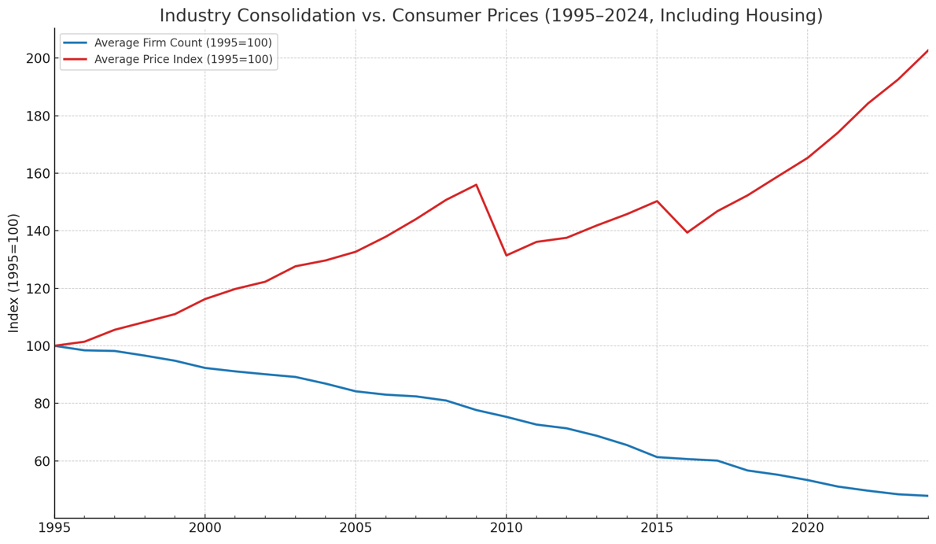

The Big Picture: Fewer Firms, Higher Prices

When we average across all seven industries, the story is unmissable: as firm counts trend down, consumer prices trend up.

This correlation doesn’t capture every nuance, but it captures the weight of the structural change in America’s economy. Consolidation has not only reshaped markets; it has reshaped our wallets.

A New Kind of Incentive

Traditional antitrust enforcement is slow, costly, and politically fraught. But what if government policy incentivized firms to cooperate instead of cutthroat competition or monopolization?

One solution: tax credits for minority stakes in peer companies within an industry. If dominant firms had financial incentives to keep smaller competitors afloat — instead of driving them under — consumers might benefit from preserved competition, more stable prices, and healthier job markets.

Conclusion: Rethinking Consolidation

The Federal Reserve may grab headlines, but the deeper story of rising costs comes from decades of unchecked consolidation. Airlines, autos, energy, food, telecom, television, and housing all tell the same tale: fewer firms, fewer jobs, and higher costs.

If policymakers want to get serious about affordability, they’ll need to look beyond interest rates and tackle the real driver — the concentrated power of industries that touch every part of American life.

About the Author

William T. Jordan, II is the founder and editor-in-chief of The Black Prospectus, a media platform dedicated to Black capital, enterprise, and economic power. With a background in financial services and data strategy, Jordan brings a critical yet thoughtful lens to stories at the intersection of business, policy, and culture. Reach him at founder@blackprospectus.com.

© 2025 Black Prospectus, LLC. All rights reserved.

This article is the intellectual property of Black Prospectus, LLC and may not be reproduced, distributed, transmitted, cached, or otherwise used, except with the prior written permission of the publisher.

For licensing, syndication, or media inquiries, contact founder@blackprospectus.com.